What partnerships, S corps and others with foreign partnership interests need to know for tax year 2021 and beyond

Key Takeaways

- The new detailed schedules must be filed by all pass-through entities with items of international tax relevance, including entities with foreign partners and international activities.

- The new schedules will create more clarity for shareholders and partners when it comes to calculating U.S. income tax liability and international-related income and deductions.

- The new schedules should not be as burdensome as skeptics believe once all of your ducks are in a row.

- However, filing correctly requires an in-depth understanding of complex international tax concepts. Don’t be a do-it-yourselfer here.

Beginning with the tax year 2021, partnerships, S corporations, and filers of Form 8865 (US persons who are partners in foreign partnerships, or entities electing to be taxed as partnerships)will be required to include the new Schedules K-2 and K-3, with their returns if they have items of “international tax relevance.” More on that definition in just a minute.

At their core, the new schedules and accompanying instructions are designed to help partnerships report certain US international tax information to their partners in a standardized format. This should make it easier for partners to compute and report their corresponding US income tax liability – and make enforcement of cross-border tax compliance easier for the IRS.

Who must file Schedules K-2 and K-3?

The new schedules must be filed by all pass-through entities with items of international tax relevance, including entities with foreign partners and international activities. Essentially, filers of Form 1065, Form 1120-S, and Form 8865 that have cross-border activities, investments, owners, or income may need to file Forms K-2 and K-3 in the upcoming year. However, pass-through entities that have no international tax items to report are not required to file the new schedules.

What drove the creation of Schedules K-2 and K-3?

Private equity funds and alternative asset management funds, including fund of funds, hedge funds, real estate funds, energy funds, and venture capital funds,— currently report their international tax information across various forms and schedules. They pass on much of the information to their partners via a hodgepodge of supplemental statements, whitepaper disclosures, pro-forma forms and/or footnotes attached to or provided with Schedules K-1.

As many of you know, the disparate statements and disclosures have no standardized format, so the partners receiving the statements and disclosures can find it hard to translate the information across various partnership investments when reporting the required information on the partner tax returns.

The new Schedules K-2 and K-3 provide partnerships with a standardized format for reporting US international tax information to their partners, including withholding and sourcing details for foreign partners and US international inclusions, or foreign attributes relevant for domestic partners.

How K-2/K-3 differ from K-1

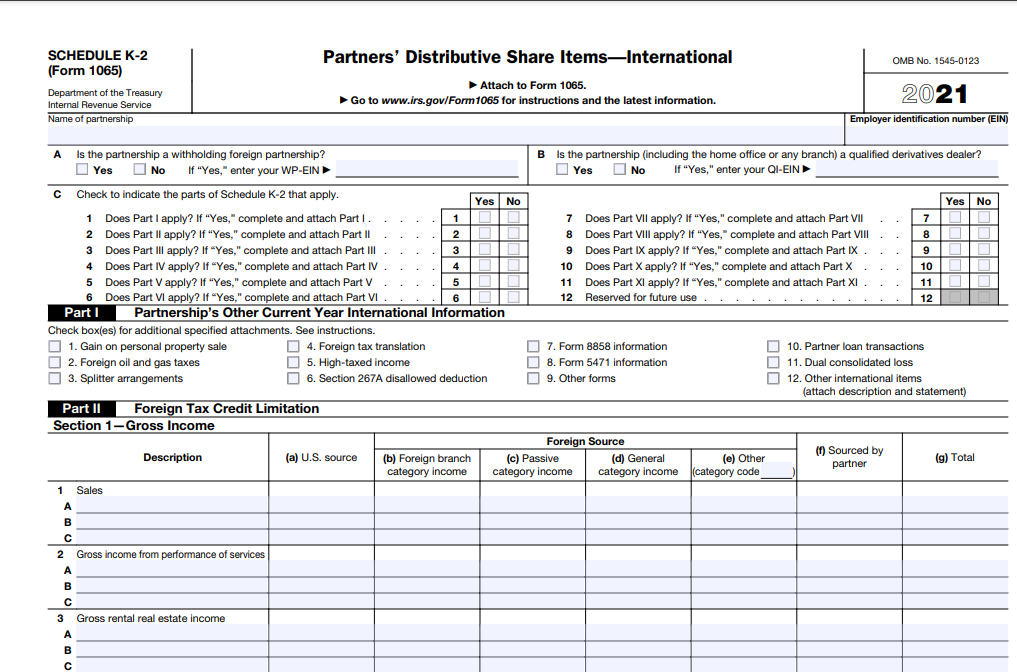

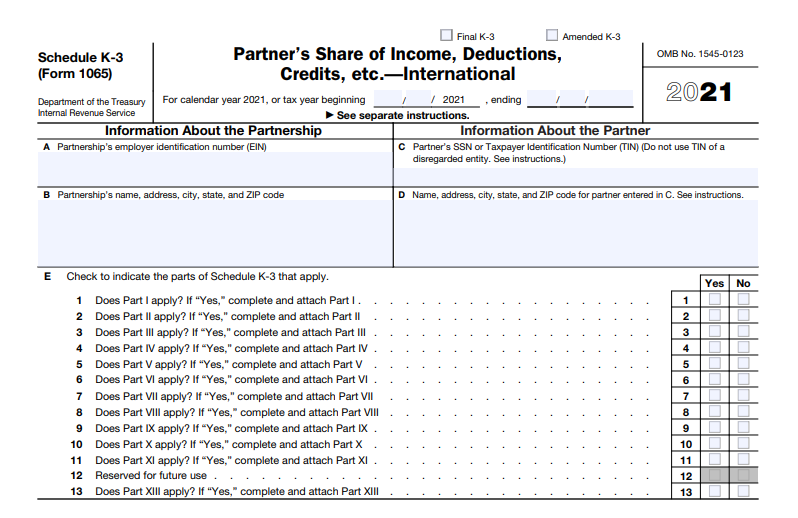

Schedule K-2 (Partners' Distributive Share Items — International) and K-3 (Partner's Share of Income, Deductions, Credits, etc. — International) will replace, supplement, and clarify the former line 16, Partners’ Distributive Share Items, Foreign Transactions, of Schedule K, Form 1065, and line 16, Foreign Transactions, of Schedule K-1 (Form 1065).

Schedules K-2 and K-3 also replace, supplement, and clarify reporting of certain amounts that were formerly reported on Form 1065, Schedule K, line 20c, Other items and amounts, and Schedule K-1, Part III, line 20, Other information.

In a nutshell, the new forms will create more clarity for shareholders and partners when it comes to calculating their U.S. income tax liability, or when considering potential international-related deductions, credits, and miscellaneous items. Much of the information to be included in Forms K-2 and K-3 was already required in Schedules K-1 via a white paper attachment. The new Schedules require filers to provide information in a standardized format and with an additional level of detail.

Clarifying ‘items of international tax relevance’

NOTE: Schedules K-2 and K-3 only apply to filers of Forms 1065, 1120-S, and 8865 that have an item of international tax relevance. While there is no concise definition of what “an item of international tax relevance” is, there is a reference to “the international provisions of the Internal Revenue Code” in the form instructions. Examples of items of international relevance that must now be reported on Schedules K-2 and K-3 (as opposed to on Schedules K and K-1) include:

- Foreign tax credit-related information including the sourcing and basketing of income and deductions including information related to items such as R&E expenses and interest expense.

- Interests in foreign entities or distributions from foreign corporations.

- Foreign partner’s U.S.-source income and/or U.S effectively connected income including distributive share of deemed sale items on the transfer of partnership interest

- Information related to

- investments in foreign entities e.g. passive foreign investment companies

- interests in controlled foreign corporations, GILTI and Subpart F income inclusions

- foreign-derived intangible income.

For example, the new Schedule K-3 provides the information that corporate and individual partners need to calculate their foreign tax credit on Form 1118, Foreign Tax Credit—Corporations, and Form 1116, Foreign Tax Credit (Individual, Estate or Trust), respectively.

The new schedules include comprehensive reporting of items related to international tax provisions within the IRC. The length of the schedules is a quick reference to the volume of information that can be required to be reported:

Schedule K-2 (Form 1065) runs 19 pages and summarizes information relevant to the partnership or S corporation.

Schedule K-3 (Form 1065) runs 20 pages and summarizes information relevant to each partner. A separate Schedule K-3 must be issued to each partner like a Schedule K-1 is. The forms may also require additional statements to be attached.

There are also separate forms and instructions for the different potential filers including a separate Schedule K-2 and Schedule K-3 for Form 1065, Form 1120-S, and Form 8865.

Treatment of undocumented partners

One thing seems to have caught many partnerships off guard. Even if they have no cross-border investments or assets, they are still required to file schedules K-2 and/or K-3 if they have foreign partners. Undocumented partners are presumed to be foreign. So, it will be important for partnerships to verify that their partners are documented via a Form W-8 or W-9.

Considerations for partnerships, fund managers and S Corporations

The new schedules will add a significant new reporting requirement for partnerships and S corporations. The forms are extensive and thus, require an in-depth understanding of complex international tax concepts. Among other items, the forms require the filer to understand sourcing rules, foreign derived intangible income (FDII) rules, dual consolidated loss rules, §267A, and the subpart F and GILTI rules among others.

Private equity and alternative asset management funds that have international activities also face a unique challenge with this new reporting requirement. The additional detail required in the new schedules may create an increased tax compliance burden for funds, investor-relations issues and timing issues related to delivering Schedule K-1s, K-2 and K-3s.

If you manage a fund, you may want to revise your timeline and deadlines associated with providing investor tax packages that include these schedules. If you manage a partnership, you may want to separate the delivery of Schedules K-1 from the new Schedules K-2 and K-3.

NOTE: The IRS announced penalty relief for the 2021 tax year for partnerships, S corporations, and other taxpayers who make a good faith effort to complete the new forms on time -- but who fall short on the new requirements (see Notice 2021-39). Despite the grace period, partnerships and S corporations will want to make plans to complete the forms properly from the outset.

Impact on partners and shareholders

Schedules K-2 and K-3 will provide welcome relief to partners, S corporation shareholders, and their advisors, who often had to interpret a variety of whitepaper statements. The new standardized format that provides information on items such as the foreign tax credit information (FTC) or information regarding passive foreign investment companies (PFICs) should alleviate some of the compliance burdens for those taxpayers. This will be especially helpful around the tax deadlines when investors that hold interests in several pass-through entities have a very short window to prepare their returns.

Partners and S corporation shareholders will want to compare the Schedules K-3 they receive this year to the Schedules K-1 they received in the prior year for new or unexpected information. If there is new information, such as indirect ownership of foreign entities that the owners of those pass-through entities were previously unaware of, then it may be prudent to confirm that no crucial information was omitted or lost in the whitepaper detail in prior years.

Conclusion

Partnerships and S corporations, as well as filers of Form 8865, should prepare for the upcoming filing requirement by ensuring their partners are properly documented with a W-8 or W-9 form, by reviewing their 2021 transactions, and by determining whether the filing requirement applies. While the new schedules are a compliance burden for pass-through entities, they will aid pass-through entity owners and IRS enforcement efforts with respect to international transactions. In the long run, that’s good for everyone.

If you have questions about Schedule K-2 or K-3 filing requirements, or if you have other questions about your international partnership interests, please do not hesitate to contact us.

===========================================

John Samtoy is a Partner in the Irvine, CA office of HCVT. John specializes in international tax consulting and compliance services and serves high net worth individuals, closely-held businesses, and private equity clients across a variety of industries. John has experience serving multinational clients immigrating to and doing business in the U.S. as well as U.S. clients working and establishing operations overseas.