U.S. businesses exporting goods to overseas customers may be underutilizing key tax incentives that could reduce their overall tax liability.

Export tax incentives encourage businesses to increase activity and hiring domestically, while expanding exports and helping the country's economy grow.

The United States offers two separate export tax incentives – the Interest-Charge Domestic International Sales Corporation (IC-DISC) regime and the Foreign Derived Intangible Income (FDII) regime – to support its companies in their international trade efforts.

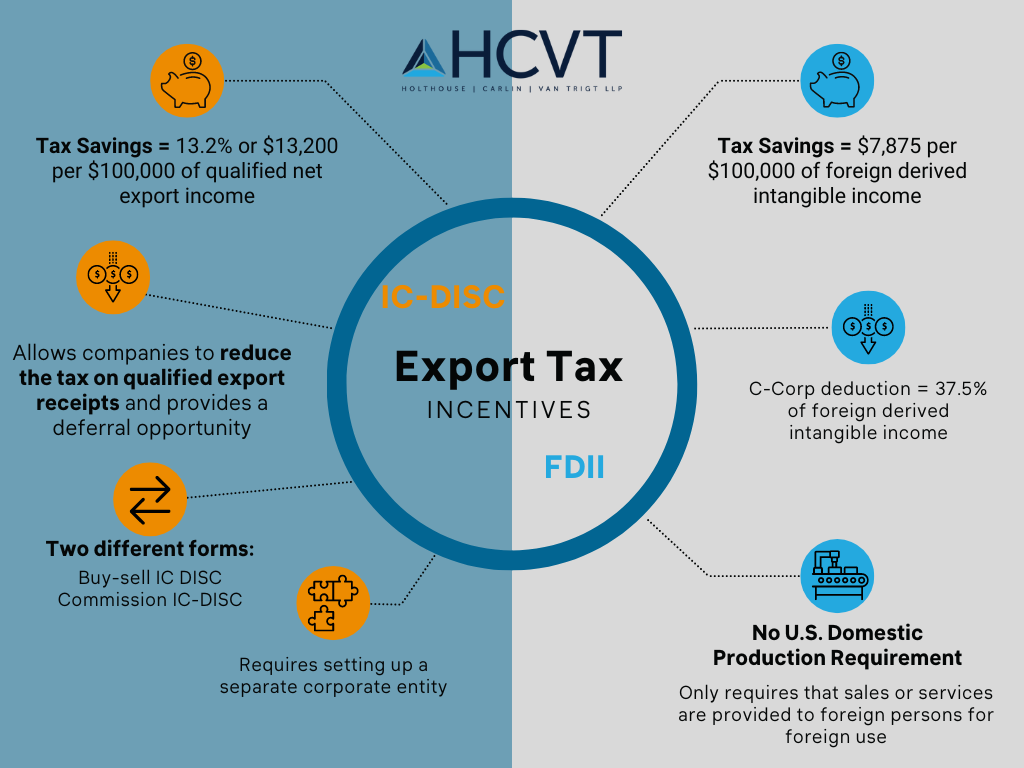

- The IC-DISC regime allows for some deferral of income but more importantly it can convert what otherwise would be ordinary income (or double taxed income in a corporate structure) to a qualified dividend that is taxed only once at a corporate level. The tax savings under this regime is 13.2% or $13,200 per $100,000 of qualified net export income.

- The FDII regime includes a 37.5% deduction for corporate taxpayers that reduces the US corporate rate from 21% down to 13.125% of foreign derived intangible income. The FDII regime results in a tax savings of $7,875 per $100,000 of foreign derived intangible income.

These regimes offer significant tax benefits that can lead to substantial savings for the businesses and their owners. The use of these regimes is encouraged by the US and is part of our tax code, and it is important for businesses and their owners to take advantage of them when applicable.

While the advantage of these tax incentives might be most easily recognized in the manufacturing and distribution industry, the opportunity for savings extends to a wider range of industries, including:

- Media & Entertainment: exporting or licensing films, television shows or other entertainment products overseas

- Technology: selling software, hardware, or other intangible products overseas or providing technology services or license technology products

- The FDII regime may provide a deduction for income from the sale of foreign-derived intangible property.

- Agriculture: exporting products overseas

- The IC-DISC regime allows agricultural businesses to defer a portion of the income earned on exports and can convert what would be ordinary income to qualified dividends saving money for the owners of agricultural businesses.

- Healthcare: exporting medical devices, pharmaceuticals, or other products overseas, or providing a service from the US to customers overseas

- Service industries: providing services to foreign clients

- Service-based companies, such as consulting firms, that provide services to foreign clients may benefit from the FDII tax incentive, which provides a deduction for income from the provision of services to foreign clients.

There are a few things to consider, when it comes to deciding whether an IC-DISC or FDII approach is best for your company.

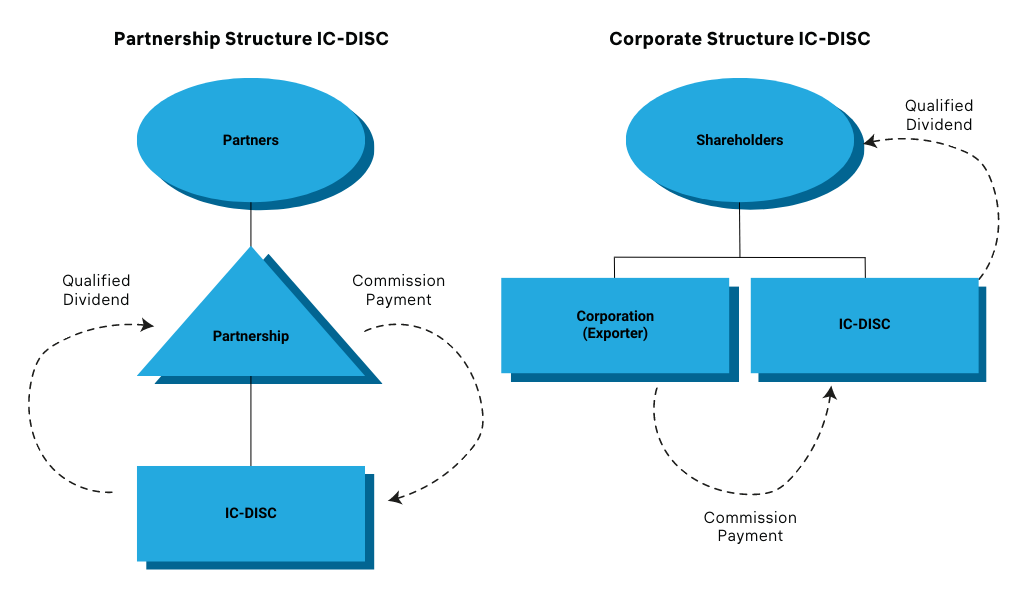

IC-DISC

An IC-DISC allows companies to reduce the tax on qualified export receipts. Qualified export receipts are receipts from sales of “export property” which include goods manufactured, produced, grown, or extracted in the U.S. and sold for use, consumption, or disposition outside of the U.S. In addition, an IC-DISC provides a deferral opportunity.

This regime can take on two forms:

- In a buy-sell IC-DISC, the IC-DISC purchases the export products from the manufacturer and then sells them to the foreign customer, earning a profit on the difference between the purchase price and the sales price.

- In a commission IC-DISC, the related exporter (manufacturer) sells the export products directly to a foreign customer, paying a commission to the IC-DISC based on the sales price of the products. The commission creates a deduction from ordinary income for the related exporter and the commission income is then taxed at the lower capital gain tax rates, which can significantly reduce the tax liability of the manufacturer.

With a commission IC-DISC, a company could set up a “paper” company with no operations that can take advantage of the IC-DISC benefits. The amount of the commission paid to a commission IC-DISC can be determined under one of three methods:

- 4 percent gross receipts method: The IC-DISC earns a commission equal to 4 percent of the gross export receipts

- 50-50 combined taxable income method: The IC-DISC earns a commission equal to 50 percent of the combined taxable income of the IC-DISC and the related manufacturer on qualified export receipts

- 482 method: The IC-DISC commission is determined based on arm’s length pricing under the principles of transfer pricing under §482 (not commonly used)

Example IC-DISC structures:

FDII

Introduced as part of the Tax Cuts and Jobs Act (TCJA), FDII was designed to encourage businesses to hire and build domestically and to subsequently export domestically produced goods and services to overseas customers.

Under this regime, a C-Corporation is allowed to take a deduction equal to 37.5% of its foreign derived intangible income, bringing the effective rate on FDII down from regular 21% corporate rate to a 13.125% tax rate. It’s important to note that this deduction will decrease for tax years beginning after 2025 to 21.875% which will result in an effective 16.4% rate.

To calculate the FDII deduction, a corporation needs to determine their foreign derived deduction eligible income (FDDEI). FDDEI includes income from sales or services provided to foreign persons for foreign use. The foreign use requirement means that the goods or services must be consumed, sold, or otherwise used outside of the U.S.

Which option is better for you?

U.S. exporters will want to make sure they are maximizing their export tax incentives between the two regimes.

The tax savings from the IC-DISC regime are more substantial, but require setting up a separate corporate entity, bringing along its own setup costs and annual maintenance requirements including maintaining separate books and filing separate tax returns.

The FDII deduction only requires that sales or services are provided to foreign persons for foreign use. There is no U.S. domestic production requirement, like we see with the IC-DISC rules where goods must be manufactured, produced, grown, or extracted in the U.S. Because of the limited rule, the FDII regime may provide a benefit on sales or services income that would not be eligible for the IC-DISC regime.

If you are currently exporting goods to overseas customers, or are considering the tax implications in doing so, now is the time to act. Please do not hesitate to contact us if you have any questions.

John Samtoy is a Partner in the Irvine, CA office of HCVT. John specializes in international tax consulting and compliance services and serves high net worth individuals, closely held businesses, and private equity clients across a variety of industries. John has experience serving multinational clients immigrating to and doing business in the U.S. as well as U.S. clients working and establishing operations overseas.