In a move that surprised many experts, the Internal Revenue Service (“IRS”) recently issued proposed regulations indicating that individuals making Section 962 elections can now take a 50 percent deduction on their GILTI income. As I wrote in my HCVT Tax Alert: New Guidance on Global Intangible Low-Taxed Income (GILTI), many in the professional community had been skeptical that individuals would be allowed to take the 50 percent deduction. So, these newly proposed regulations provide much-needed relief for individual taxpayers.

Individuals making the 962 elections are also allowed to take an indirect foreign tax credit of 80 percent of foreign taxes paid in addition to the 50 percent deduction. When taken together, the new deduction and the credit could eliminate the U.S. tax on GILTI for some individuals and it could allow other individuals to reduce their GILTI liability significantly. The individual making the 962 elections can potentially defer their U.S. tax liability on foreign corporate earnings until profits are distributed. This makes the 962 elections the key planning technique that individual direct owners of controlled foreign corporations (CFCs) need to consider first.

What is GILTI?

GILTI rules, which were introduced as part of the 2017 Tax Cuts and Jobs Act (“TCJA”), ushered in a new anti-deferral regime. At a high level, GILTI refers to any income earned by a CFC (above a 10 percent return on fixed depreciable assets) that is not already subject to U.S. tax. United States taxpayers are required to include GILTI on their U.S. tax returns and are required to pay tax on that income even though the money hasn’t been distributed from the CFC. This situation creates “phantom income” which U.S. taxpayers are taxed on, even though they don’t have the cash in hand to pay that tax liability.

Example: Karen owns ABC Corporation (“ABC”), which is an S-Corporation for U.S. tax purposes. ABC specializes in digital animation. ABC owns 100 percent of a corporation in India (“ABC India”). ABC contracts with companies that need animation work done and outsources some of that work to ABC India. ABC India’s income is composed entirely of income earned from performing animation services in India. None of ABC India’s income is considered Subpart F income.

Before passage of tax reform in 2017, none of ABC India’s income would have been subject to U.S. tax unless ABC India distributed its income to ABC. Today, ABC is required to include GILTI from ABC India on its U.S. tax return even though ABC India has not made a cash distribution to ABC. GILTI from ABC India is equal to ABC India’s earnings and profits (E&P)(less a 10 percent return on ABC India’s fixed depreciable assets). Because ABC is an S-corporation, Karen is required to include the company’s GILTI on her personal income tax return. Karen must treat the GILTI as ordinary income that is subject to graduated tax rates up to the 37 percent rate.

Many closely held businesses need to keep their profits overseas in order to expand and to reinvest. As a result, the relatively high tax rate on phantom income is a burden for U.S. taxpayers. The tax on GILTI is, therefore, a key issue that closely-held businesses like ABC, which have overseas operations, will need to manage.

The 962 Election

The 962 election allows individuals to elect to be taxed on deemed income from CFCs as though those individuals are corporations. The deemed income that the 962 election applies to includes income under section 951(a), Subpart F income, 956 investments in U.S. property, and GILTI income.

When individuals make a 962 election, a theoretical U.S. corporation is interposed between the individual and the CFC for purposes of section 951(a) income only. Individuals making the election include an “election statement” with their individual tax returns along with a computation showing the amount of income, the US corporate tax liability on that income (computed under section 11), the foreign tax credit allowable, and their 962 liability.

The 962 elections have been in the tax code for years, but it has seldom been applied. That’s because the 962 elections could expose a U.S. taxpayer to double taxation. When an actual distribution of 951(a) profits is made from a CFC (profits subject to tax under 962) then the U.S. individual is subject to tax on that income less any U.S. taxes he or she paid. That way, the individual is taxed once as a theoretical U.S. corporation under 962 and is taxed a second time as an individual when a dividend is actually paid. This treatment is intended to mimic the effects of having the stock of the CFC held by an actual U.S. corporation. In that scenario, the U.S. corporate tax would be paid and then the individual would include the dividend from the U.S. corporation once distributed.

Why individuals must consider the 962 elections post-tax reform

The 962 election is now more appealing than ever thanks to the TCJA, which reduced the corporate tax rate to 21 percent from 35 percent. The new tax rate, combined with the 50 percent deduction on GILTI, means that U.S. corporations pay an effective tax rate of 10.5 percent on their GILTI income from CFCs. Taking into account the 80 percent indirect foreign tax credit, a U.S. corporation now owes no taxes on its GILTI as long as there is at least a foreign corporate tax of 13.125 percent imposed on its GILTI. The newly proposed regulations make it clear that individuals receive the same tax treatment as corporations when it comes to making a 962 election.

Individual taxpayers may owe no current tax on GILTI when they make a 962 election. This allows them to defer their U.S. tax liability on GILTI until they receive a distribution from the foreign corporation. When an actual distribution is made by the corporation, taxpayers may also be able to treat the distribution as a qualified dividend that is subject to the preferential 20 percent tax rate, not the 37 percent rate they would pay on GILTI. So, an individual may be able to defer the payment of tax and realize permanent tax savings by making the 962 elections.

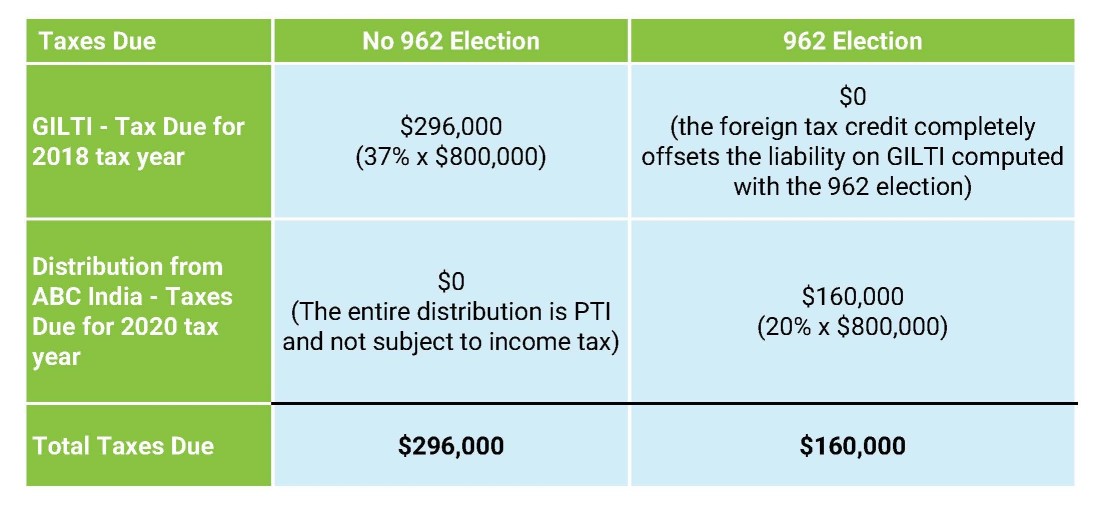

Example: Continuing our earlier example, let’s say ABC India has no depreciable assets, and it has $800,000 of post-tax E&P in 2018. Let’s say ABC India paid $200,000 of taxes on that income in India is 2018. In 2020 ABC India will distribute the $800,000 in profits to ABC. Let’s assume Karen is subject to the highest marginal tax rate in the U.S. and that ABC India is the only CFC in which both ABC and Karen have an interest. For simplicity, let’s assume there is no change in the exchange rate between 2018 and 2020.

In the above example, ABC would have a GILTI inclusion of $800,000. Because ABC is an S-corporation, that income would be reported on Karen’s individual U.S. tax return.

SCENARIO 1: If Karen DOES NOT make a 962 election, she would pay tax on the $800,000 GILTI inclusion at the ordinary 37 percent rate. Her U.S. tax liability on the inclusion would be $296,000 (37% of $800,000). When ABC India actually distributed the $800,000 in profit in 2020, the entire amount would be considered previously taxed income (“PTI”) and would not be subject to U.S. federal income tax again (although it would be subject to the net investment income tax or “NIIT”).

SCENARIO 2: If Karen DOES make a 962 election, she would compute the tax liability on the $800,000 GILTI inclusion as though she were a U.S. corporation. She would be required to “gross up” the $800,000 for the $200,000 of foreign taxes paid. She would then be required to calculate the corporate income tax liability on $1 million of GILTI. To do this, Karen would first take the 50 percent deduction of $500,000 (i.e. 50% of $1 million) leaving her with $500,000 of theoretical corporate income. She would then calculate the corporate tax due of $105,000 (i.e. 21% of $500,000) before the foreign tax credit. Next, Karen would take the foreign tax credit allowed for GILTI of $160,000 (i.e. 80% of $200,000) and use it to offset the corporate tax due.

Because the foreign tax credit is more than the corporate tax due, Karen would owe no taxes on GILTI under her 962 election. When ABC India actually distributed the $800,000 in profit in 2020, the entire amount would be subject to tax as a qualified dividend at a 20 percent rate. Karen’s tax due on the distribution is $160,000 (i.e. 20% of $800,000) before taking into account NIIT.

|

|

|

By making the 962 elections, Karen was able to defer paying U.S. tax on the income of ABC India and realize a permanent savings of $136,000!

Conclusion

TCJA’s international provisions present a challenge for individuals and their closely-held businesses. The newly proposed regulations, which allow a 50 percent deduction on GILTI for individuals making a 962 election, provide much-needed relief to individual U.S. taxpayers. Calculating GILTI and making 962 elections are complex. They may not be the best options for all U.S. taxpayers. For example, taxpayers with CFCs that pay low (or no) taxes may be subject to double taxation and higher overall effective tax rates on GILTI income and the related earnings if they make a 962 election.

If you or a colleague has questions about the impact of GILTI or on the 962 elections please don’t hesitate to contact me at (714) 361-7685 or John.Samtoy@hcvt.com.

John Samtoy is a Tax Principal in the Irvine, CA office of HCVT. John specializes in international tax consulting and compliance services and serves high net worth individuals, closely held businesses, and private equity clients across a variety of industries. John has experience serving multinational clients immigrating to and doing business in the U.S. as well as U.S. clients working and establishing operations overseas.