The Treasury Department’s “final” GILTI regulations issued in late June could lead to amended partnership returns, amended 2018 K-1s, and confused investors. These new regulations apply retroactively to years beginning in 2018. Bottom line: The final GILTI regs are coming out just when several new provisions of the Tax Cuts and Jobs Act (“TCJA”) become effective for the first time. Needless to say, this will add complexity to an already challenging extended tax deadline.

Aggregate approach

The final regulations state that an aggregate approach must be used by domestic partnerships and S-corporations (together hereinafter referred to as “domestic partnerships” for purposes of brevity) with respect to Global Intangible Low-Taxed Income (GILTI). Under the aggregate approach, domestic partnerships are not treated as U.S. shareholders for the purposes of applying Section 951A only. Instead, domestic partnerships are treated as aggregate entities, the same way foreign partnerships are treated for section 958(a) purposes. As a result, domestic partnerships will not determine GILTI at an entity level. Instead, domestic partnerships will pass on information about tested income and tested loss to their partners and shareholders.

Only 10 percent of U.S. shareholders of controlled foreign corporations (CFCs) take tested income and tested loss into account to determine GILTI inclusions. Partners and shareholders that are U.S. shareholders of CFCs through domestic partnerships will need to consider their allocable share of tested income and tested loss in order to compute GILTI at an individual or corporate level. This applies only if they are “U.S. shareholders” of the underlying CFCs. If they are not U.S. shareholders—i.e. they are less than 10-percent owners of the CFC--then they will not have to take those items into account. Further, they will no longer have a GILTI inclusion from the domestic partnerships in which they invest.

These final regulations, issued in June 2019, apply retroactively for the tax year 2018 and they are a significant departure from the proposed GILTI regulations that were issued on October 10, 2018. Those previously proposed regulations provided for a hybrid approach (see below).

Hybrid approach

Under the hybrid approach, domestic partnerships that are U.S. shareholders of a CFC were required to compute the GILTI inclusion at the partnership level. Under this approach, U.S. partners, who were not U.S. shareholders of the CFC, were required to include their allocable share of the partnership’s GILTI inclusion as income.

The partners who were U.S. shareholders of the CFC were treated as though they proportionately owned the stock of the CFC. Those U.S. shareholder partners determined their share of GILTI under the method described under the aggregate approach.

A number of domestic partnerships have already issued 2018 K-1s with GILTI computed under the hybrid approach. Partners who received K-1s that included GILTI should NOT report the GILTI income based on these final regulations. Those partners should verify whether or not the domestic partnerships will be issuing amended K-1s based on these final regulations. If the domestic partnerships will not be issuing K-1s, then the partners should consider filing Form 8082 to disclose the inconsistent treatment of GILTI.

For partners trying to determine if GILTI is in fact reported on their K-1s, they can look for income reported on line 11F (from a partnership) or line 10E (from an S-corporation). Language similar to the following may also appear in the K-1 footnotes when there is a GILTI inclusion being reported: “YOUR DISTRIBUTIVE SHARE OF THE PARTNERSHIP’S INCLUSION UNDER SECTION 951A IS REFLECTED ON YOUR SCHEDULE K-1, PART III, LINE 11F, SECTION 951A INCOME”.

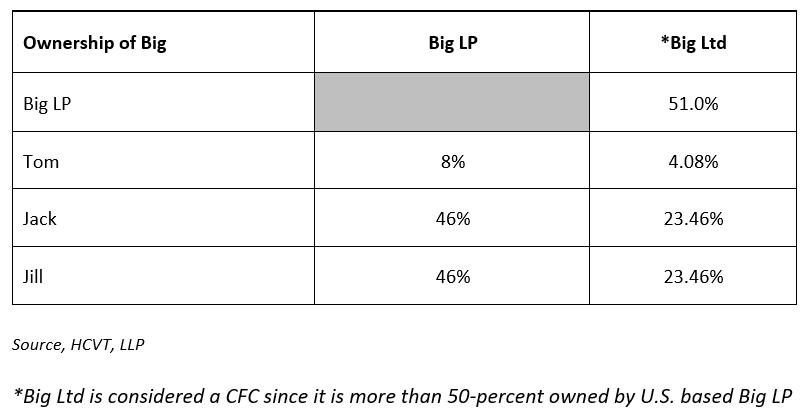

Example

Big Investment Partners LP (“Big LP”), is a U.S. partnership that owns 51 percent of Big Ltd a Cayman Islands corporation. The other shareholder is of an unrelated foreign person.

Big LP has three partners--Jack, Jill, and Tom—each of whom is a U.S. person. Jack and Jill own 46 percent of Big LP each and Tom owns the remaining 8 percent. Jack, Jill, and Tom are not related to each other.

In this case, Big Ltd is considered a CFC because a U.S. shareholder (Big LP), owns more than 50 percent of Big Ltd’s stock. Big LP must file a Form 5471 since it is a Category 1, 4, and 5 U.S. shareholder of Big Ltd. However, Big LP does not have a GILTI inclusion that is allocated to its U.S. partners. That’s because, under the new regulations, an aggregate approach is used. As a result, Big LP is not treated as a U.S. shareholder for purposes of 951A, including the computation of the GILTI inclusion.

Big LP determined its taxable income and issued K-1s to its partners on April 14th, 2019. At the time, Big LP relied on the proposed GILTI regulations from October 2018 to determine its GILTI inclusion. As a result, GILTI income was reported on line 11F. Big LP also included information about each partner’s allocable share of tested income from Big Ltd on the K-1s that were issued to the other partners.

As mentioned earlier, Tom owns 8 percent of Big LP and indirectly owns 4.08 percent of Big Ltd. Tom is not a U.S. shareholder of Big Ltd. Therefore, Tom should not include his share of tested income from Big Ltd. Additionally, under the new final regulations, Big LP should not have determined GILTI at the partnership level. So, Tom should not include the GILTI reported on line 11F of the K-1 that was issued to him by Big LP on his Form 1040. However, Tom should ask whether Big LP will be issuing amended K-1s that take the final regulations into account. If Big LP is not issuing amended K-1s, then Tom should file Form 8082 with his Form 1040. That way he can disclose the inconsistent treatment of the GILTI income that’s reported on line 11F of the K-1 he received.

Jack and Jill each indirectly own 23 percent of Big Ltd. Jack and Jill are U.S. shareholders of Big Ltd. Big Ltd is also considered a CFC because Big LP owns more than 50 percent of Big Ltd and because Big LP is treated as a U.S. shareholder of Big Ltd. Jack and Jill each consider their allocable share of tested income from Big LP and determine their GILTI inclusion on their respective 1040s. There is no change to Jack’s or Jill’s reporting under the new regulations.

Next steps

Partners of U.S. partnerships and shareholders of S corporations may have already received K-1s for 2018 that allocated GILTI inclusions prior to the June 21st, 2019 issuance of those final regulations. These partners may want to contact the partnership or S-corporation to determine whether the entity plans to issue an amended K-1. If the entity does not plan to issue an amended K-1, then those partners or shareholders may need to file Form 8082 with their tax returns. Form 8082 would indicate that according to the final GILTI regulations, there is no inclusion needed for partners or shareholders that own less than 10 percent of the underlying CFC.

Partnerships and S-corporations that issued K-1s may want to determine if they will file amended returns and reach out to partners and shareholders proactively. This will allow them to address the change in the GILTI rules and it will also help to avoid a last-minute scramble at the extended filing deadline.

Conclusion

The final GILTI regulations which apply retroactively to tax years beginning in 2018 are a significant departure from the previously proposed regulations. A number of domestic partnerships and S-corporations issued 2018 K-1s prior to when those final GILIT regulations were issued. Those entities will now be faced with a decision about whether to amend their 2018 reporting or simply to report correctly prospectively.

Partners and shareholders that received K-1s (with GILTI included) will want to contact the domestic partnerships and S-corporations that issued those K-1s so they can verify whether or not amended K-1s will be issued. If amended K-1s will not be issued, then a Form 8082 can be filed to report the inconsistent treatment of GILTI.

These changes ultimately provide relief for taxpayers. However, the timing of the new rules adds to the complexity of reporting at the filing deadline. It goes without saying that it will be a significant compliance challenge for both partners and partnerships.

If you or a colleague have questions about the impact of GILTI on your 2018 return please don’t hesitate to contact me at 714-361-7685 or John.Samtoy@hcvt.com

John Samtoy is an International Tax Principal in the Irvine, CA office of HCVT. John specializes in international tax consulting and compliance services and serves high net worth individuals, closely-held businesses, and private equity clients across a variety of industries. John has experience serving multinational clients immigrating to and doing business in the U.S. as well as U.S. clients working and establishing operations overseas.